Choosing a financial advisor is one of the most consequential decisions you’ll make for your family’s financial future. The right advisor can help you navigate complexity, work to mitigate costly mistakes, and build a plan that may last well beyond your own lifetime.

The challenge is that most people don’t know what to ask when they sit down across the table, or that they should be asking hard questions at all.

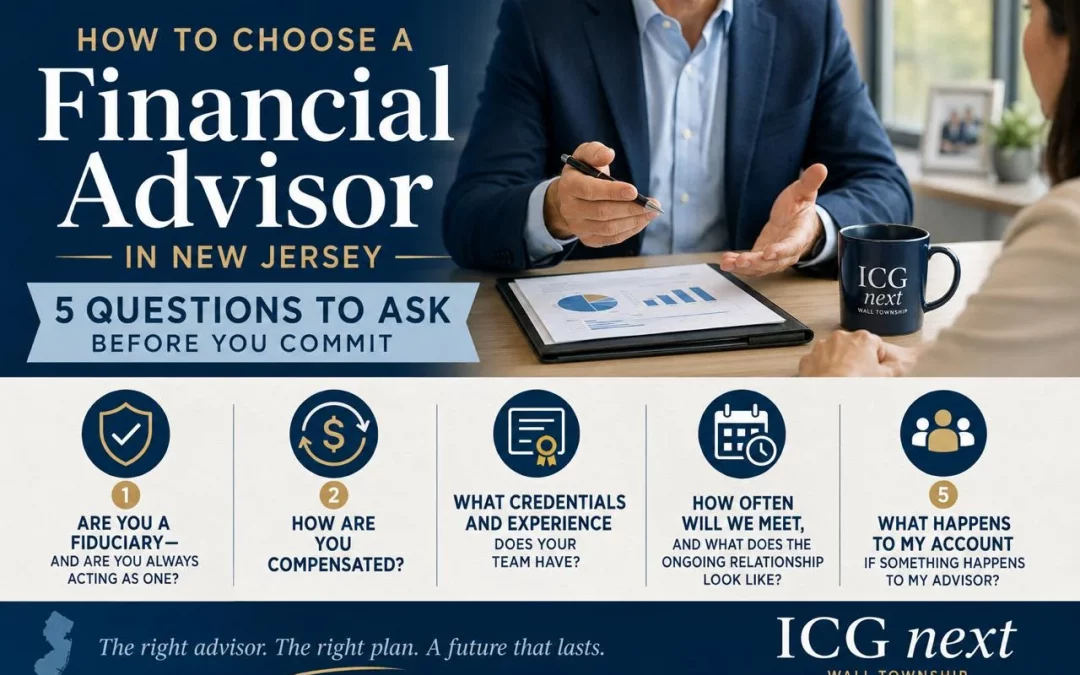

Here are five specific, concrete questions worth bringing to any initial conversation with a financial advisor, along with context for what good answers actually look like.

1. Are You a Fiduciary — and Are You Always Acting as One?

This is the most important question on the list. Some advisors are registered both as investment advisors and broker-dealers. When acting in the broker-dealer capacity, they may not be held to the same fiduciary standard, which means the obligation to act in your best interest doesn’t necessarily apply to every interaction.

Under the fiduciary standard, the SEC requires both a duty of care and a duty of loyalty, the latter meaning the advisor must not subordinate your interests to their own, and must make full and fair disclosure of conflicts of interest with enough specificity for you to make an informed decision.

Ask directly: Are you a fiduciary? In all situations, or only some? What happens when a conflict of interest arises? A thoughtful, specific answer to all three parts of that question is a good sign.

2. How Are You Compensated?

Compensation structure is one of the clearest windows into how an advisor’s interests align or don’t align with yours. There are a few common models worth understanding.

Commission-based advisors earn money when they sell you a product, which can create a potential tension between their compensation and what is most appropriate for your situation. Fee-only advisors charge a flat fee, hourly rate, or percentage of assets under management. Fee-based advisors may combine both models, earning an advisory fee while also earning commissions in some circumstances.

ICG next primarily uses an assets-under-management fee structure, a single flat quarterly fee disclosed on account statements, with no commissions, loads, or transaction charges on securities. The advisor’s compensation is tied to the value of the client’s account over time rather than to individual transactions, designed to help align the firm’s interests with yours.

Whatever model a prospective advisor uses, they should be able to explain it clearly in plain language. If the explanation is evasive or overly complicated, that’s worth noting.

3. What Credentials and Experience Does Your Team Have?

Financial advising is a broad field with a wide range of professional designations, and not all of them require the same level of education, examination, or ongoing ethics standards.

The CFP (Certified Financial Planner) designation requires completion of certified coursework through a CFP Board Registered Program, passage of a comprehensive exam, a minimum of 4,000 to 6,000 hours of professional experience, and 30 hours of continuing education every two years, including a mandatory ethics component.

Other meaningful credentials include the CIMA (Certified Investment Management Analyst), ChFC (Chartered Financial Consultant), CLU (Chartered Life Underwriter), RICP (Retirement Income Certified Professional), and CDFA (Certified Divorce Financial Analyst), each with its own educational and examination standards.

ICG next’s advisory team carries an extensive range of these designations — CFP, CIMA, ChFC, CLU, CRPC, RICP, CDFA, AIF, reflecting deep and varied expertise across the disciplines that comprehensive financial planning requires. Team members hold degrees in economics, finance, accounting, and business management.

Ask any prospective advisor about their credentials, what each one required to earn, and how they stay current. A well-credentialed team should be able to explain the value of their designations clearly.

4. How Often Will We Meet, and What Does the Ongoing Relationship Look Like?

One of the most common concerns about financial advisory relationships is that they become infrequent and impersonal after the initial account setup. Annual reviews, at best, are the norm at many firms. That cadence is rarely sufficient for families managing complex, evolving financial situations.

Ask a prospective advisor to describe their client service model in detail. How often will you meet formally? Who is your point of contact for day-to-day questions? How quickly are calls and emails returned?

ICG next’s client service policy includes a minimum of annual formal review meetings (with a preference for two per year plus a check-in call), quarterly and monthly newsletters, phone calls returned within 24 hours, emails answered within 48 hours, and summary letters within seven days of every formal meeting. Clients also have access to a dedicated administrative staff person who serves as liaison between the client and the advisory team.

A firm that can describe its service standards in concrete terms has thought carefully about what the ongoing relationship should look like. One that offers vague assurances of responsiveness without specifics probably hasn’t.

5. What Happens to My Account If Something Happens to My Advisor?

This question rarely gets asked in first meetings, but it should be near the top of the list, especially for families planning over decades. Advisors retire, change firms, become ill, or pass away.

According to a SmartAsset survey of over 460 financial advisors, roughly one in three advisors still did not have a formal written succession plan as of 2022 — and only about one in four clients ever asks their advisor about it.

The scale of the challenge is significant: Cerulli Associates estimates that approximately 109,000 financial advisors will retire between 2024 and 2034, collectively managing a substantial portion of total industry assets, raising real continuity questions for clients across the industry.

ICG next maintains a written, formal succession plan between its managing partners, advisors, and LPL Financial. The firm’s advisor-to-client ratio of 125 to 1, compared to an industry average exceeding 400 to 1, is designed to help ensure that in the event of a transition, the level of service clients have come to expect continues without interruption.

For any advisor you’re considering, ask: Do you have a written succession plan? What specifically happens to my accounts and my relationship with the firm if you are no longer able to serve me?

One More Thing: Consider the Relationship Itself

The five questions above are practical tools for evaluating competence, alignment, and professionalism. But the decision also comes down to something harder to quantify: whether you feel heard and understood by the person across the table.

Financial planning involves sharing information that is deeply personal your income, your debts, your family relationships, your concerns, your ambitions. You are entering a long-term relationship with someone who will help you navigate some of the most significant decisions of your life.

ICG next was founded in part because the team repeatedly saw friends and family struggling to find guidance they could have confidence in. That origin shapes a firm culture where advisors are expected to educate clients in plain language, take time to understand their full situation, and build relationships that extend across generations.

The right advisor makes complex things understandable, respects your intelligence, and takes the time to make sure you feel comfortable with every decision. That standard is worth holding any prospective advisor to at ICG next or anywhere else.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.