As China emerged a year ago from the shadow of the stringent zero COVID-19-related measures that all but shut down its economy for over two years, much was expected in terms of its economic growth prospects. There were numerous reports suggesting the world’s second largest economy would ignite a bout of inflation as its industrial base would require vast quantities of commodities to power a newly energized China. Clearly that didn’t happen. Here we explore why and provide our updated thoughts on investing in China and emerging markets.

Revisiting China, 2024

To be sure, coming out of the pandemic, consumers initially enjoyed spending money as everyday life normalized, and China’s electric vehicle (EV) powerhouse, BYD Company Ltd. (BYD), ratcheted up production considerably. By the end of 2023, BYD had begun to challenge Tesla’s dominance in the EV global market.

Still, as 2024 began, endemic problems remained with the property sector mired in debt, the shadow banking system (non-bank lending) showing signs of financial strain, and unemployment among the country’s youth hovering over 20%.

Moreover, a raft of economic and political/military issues are cause for concern as global investors have looked elsewhere for direct investment opportunities. Flows into China’s public companies have been hampered by questions regarding regulations that seem to fluctuate on political whims.

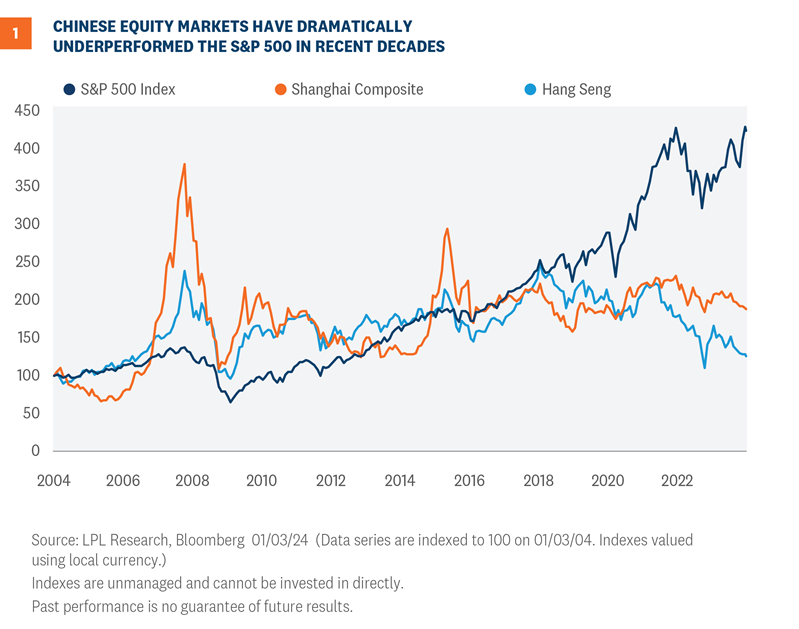

Analysts and investors seek answers as to how President Xi Jinping intends to galvanize the country’s domestic economy and once again attract global investors after dramatic underperformance by Chinese stocks relative to the U.S. in recent decades (Figure 1).

Expectations for 2024

Unexpectedly, the Third Plenum conference for 2023 was delayed last year without a suggestion of when the meeting will be held. The annual plenum is considered the most important gathering of its Central Committee officials, during which plans are set forth covering social, economic, and geopolitical goals.

Given the economic problems facing the country, coupled with an ongoing purge of officials in all spheres of economic and military activity, the postponement without formal commentary is telegraphing that the upper ranks of the party leadership are having difficulty providing a template for viable growth.

In his widely followed annual year-end address on December 31, President Xi Jinping referenced the challenges and headwinds facing the country, “Some enterprises had a difficult time. Some people had difficulty finding jobs and meeting basic needs.” He stressed that “All these remain at the forefront of my mind,” and “We will consolidate and strengthen the momentum of economic recovery.”

Xi, who has criticized the earlier decades of double-digit economic growth that were underpinned primarily via debt, has continuously mentioned the need for “high-quality development,” which wouldn’t require a heavy debt burden or the “disorderly expansion of capital.”

An influential Communist Party newspaper recently referred to the types of businesses associated with “high-quality development,” noting “advanced manufacturing, the digital economy and core technology breakthroughs” as representing what is needed for future development.

Although analysts hope that ultimately a wide-scale, fiscally funded infrastructure project will be introduced, so far, a targeted monetary approach has been the primary tool for supporting the economy. Expectations are high that the People’s Bank of China (PBOC) will cut interest rates further this year to help the ailing property market re-structure loans, but also to offer incentives for consumers across China to purchase more housing and vehicles.

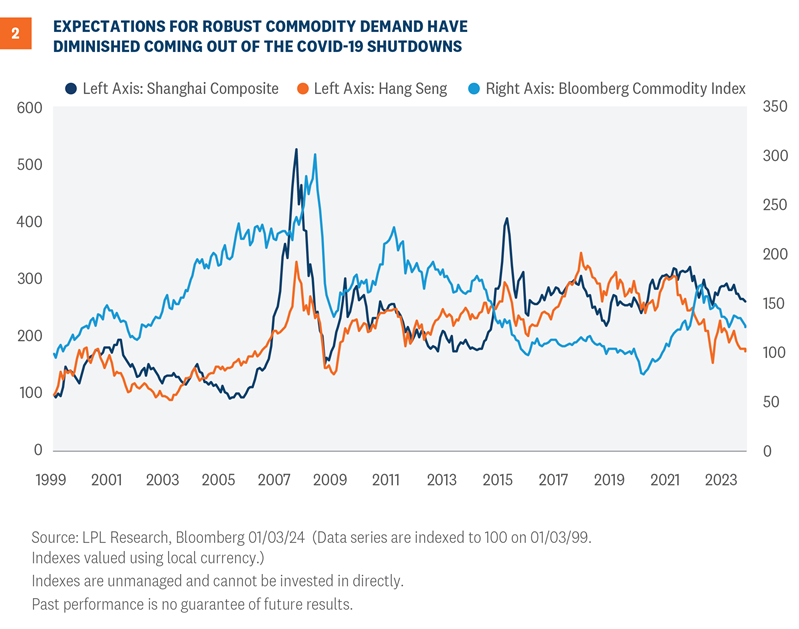

Growth forecasts remain similar to 2023, “at around 5%,” which has not been enough to get global commodities markets going (Figure 2). When the plenum does take place, there could be important adjustments to 2024 targets.

A Litany of Regulatory Concerns

For investors in Chinese markets, concerns over regulatory changes and requirements are paramount. Foreign companies have been subject to unexplained audits, while local analysts have been warned not to issue negative reports on a wide range of subjects. Unemployment data is now considered embargoed.

The move towards prohibiting the use of foreign smart phones within government offices was viewed as an attempt to thwart Apple’s hold on the local market, while propping up China’s smartphone maker Huawei. A deepening paranoia over spying apparently also played a role in Beijing’s mandate.

More recently, the arbitrary nature of the way rules and regulations are introduced was captured in new edicts for the country’s highly profitable online gaming industry announced in December. Draft restrictions on spending money and time involving online games caused an $80 billion selloff in the top names associated with the industry, notably Tencent Holdings (TCEHY) and NetEase (NETTF), followed by selling of European companies that had stakes in the Chinese firms.

Regulators quickly did an about-face to restore confidence, ultimately firing the regulator who issued the restrictions. Investigations into the country’s technology companies have also deterred serious investors.

Geopolitical Disquiet Hinders Confidence

Prominent in the list of concerns for investors is Beijing’s intentions towards Taiwan, about which Xi has been markedly clear: “The reunification of the motherland is a historical inevitability.” Assessments by intelligence experts have commented that Xi’s goal is to have the military capability to take over Taiwan by military means by 2027 and is a major reason for the ongoing purges within China’s military complex.

With Taiwan’s presidential election upcoming on January 13, Beijing will be able to assess if pro-Beijing parties gain popularity, affording Beijing the opportunity to try and bolster enough local political support to allow a “friendly” takeover. Increasingly, analysts are moving up the date for a military takeover if Taiwanese local support diminishes.

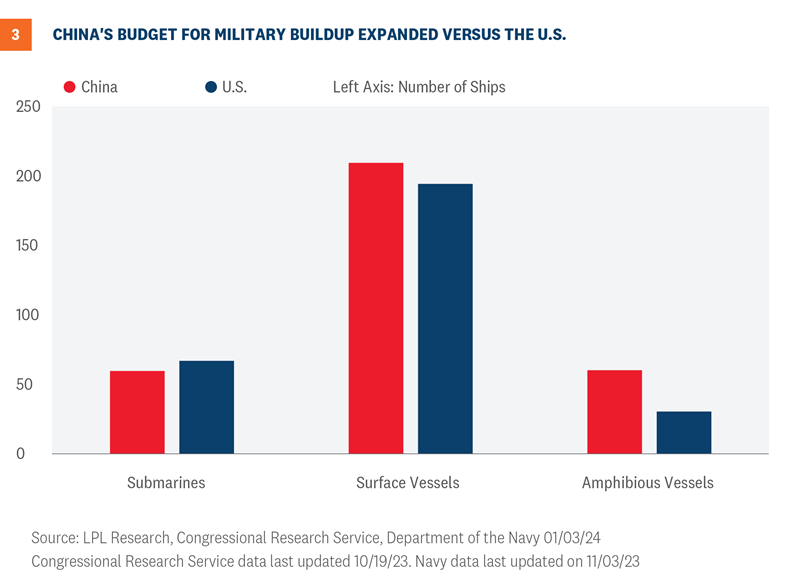

Beijing’s military activity in the South China Sea is also causing consternation for Asian nations, with the U.S. responding with an increased naval presence in the region (Figure 3).

Attractive Valuations vs. Unattractive Economic and Policy Narrative

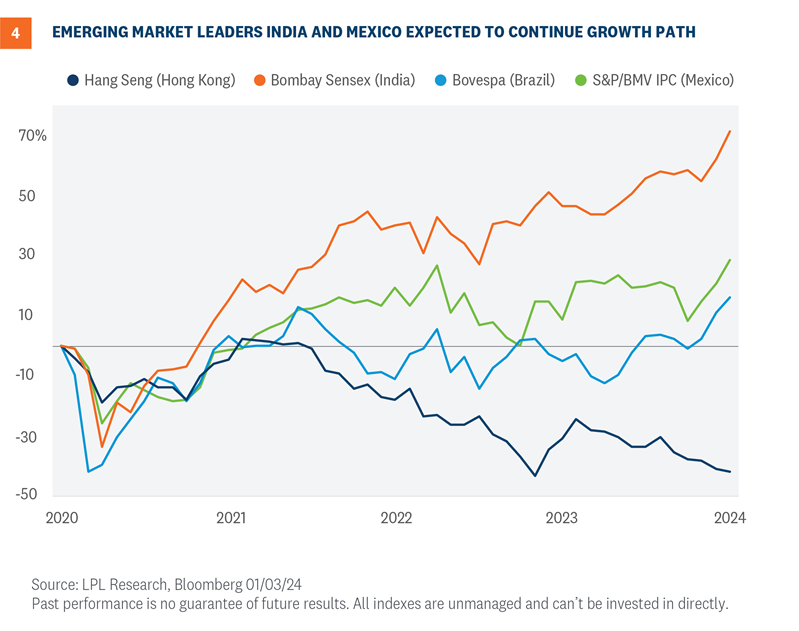

Certainly, the valuation on the Chinese stock market is attractive by any measure; however, the magnitude of overriding concerns helps explain why global investors have shifted their focus away from China and towards other emerging markets (EM), notably India and Mexico, which has benefitted from the U.S. near-shoring trend (Figure 4).

Institutional money managers have increasingly positioned clients towards Japan for an Asian allocation, rather than invest in a market stunted by capricious policy leadership, and entrenched problems in the property market and shadow banking system.

Playing Emerging Markets

LPL Research maintains its overall cautious view toward EM equities, represented by the MSCI EM Index. EM does, however, offer select attractive opportunities, particularly now that the Federal Reserve and European Central Bank’s interest rate hiking cycles are presumably over, as global financial conditions ease in concert with a weaker U.S. dollar.

We encourage the use of active management in the space to help distinguish among the heterogeneous composition of the EM universe. EM dispersion has been particularly high over the past few months, with the MSCI China Index down 5.9% since September 30, 2023, while the MSCI EM Index Ex. China has gained 10.8% and outperformed the S&P 500 during that time.

Investment Conclusion

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) recommends a neutral tactical allocation to equities, with a modest overweight to fixed income funded from cash. The risk-reward trade-off between stocks and bonds still looks relatively balanced to us even after the strong late-year rally, with core bonds providing a yield advantage over cash. The Committee favors U.S. equities over international and EM, but within EM, maintains a positive outlook for Latin America and India.

The STAAC recommends large cap growth style equities over their large cap value counterparts. The Committee believes growth style large-cap equities may benefit from lower inflation and stabilization of interest rates in the intermediate term. Growth stocks may also benefit from superior earnings prospects against a backdrop of a slowing economy.

Within fixed income, the STAAC recommends an up-in-quality approach with benchmark-level interest rate sensitivity. We think core bond sectors (U.S. Treasuries, agency mortgage-backed securities (MBS), and short-to-intermediate maturity investment grade corporates) are currently more attractive than plus sectors (high-yield bonds and non-U.S. sectors), except for preferred securities, which appear attractive after having sold off last spring due to stresses in the banking system.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Value investments can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time.

The prices of small cap stocks are generally more volatile than large cap stocks.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

LPL Financial does not provide investment banking services and does not engage in initial public offerings or merger and acquisition activities.

For a list of descriptions of the indexes and economic terms referenced in this publication, please visit our website at lplresearch.com/definitions.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered inv estment advisor and broker -dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment a dvice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

| Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value |

RES-000524-1223 | For Public Use | Tracking #524422 (Exp. 01/2025)